How China Outmaneuvered Trump at the Busan Summit

Trump won the headlines; Xi kept the leverage

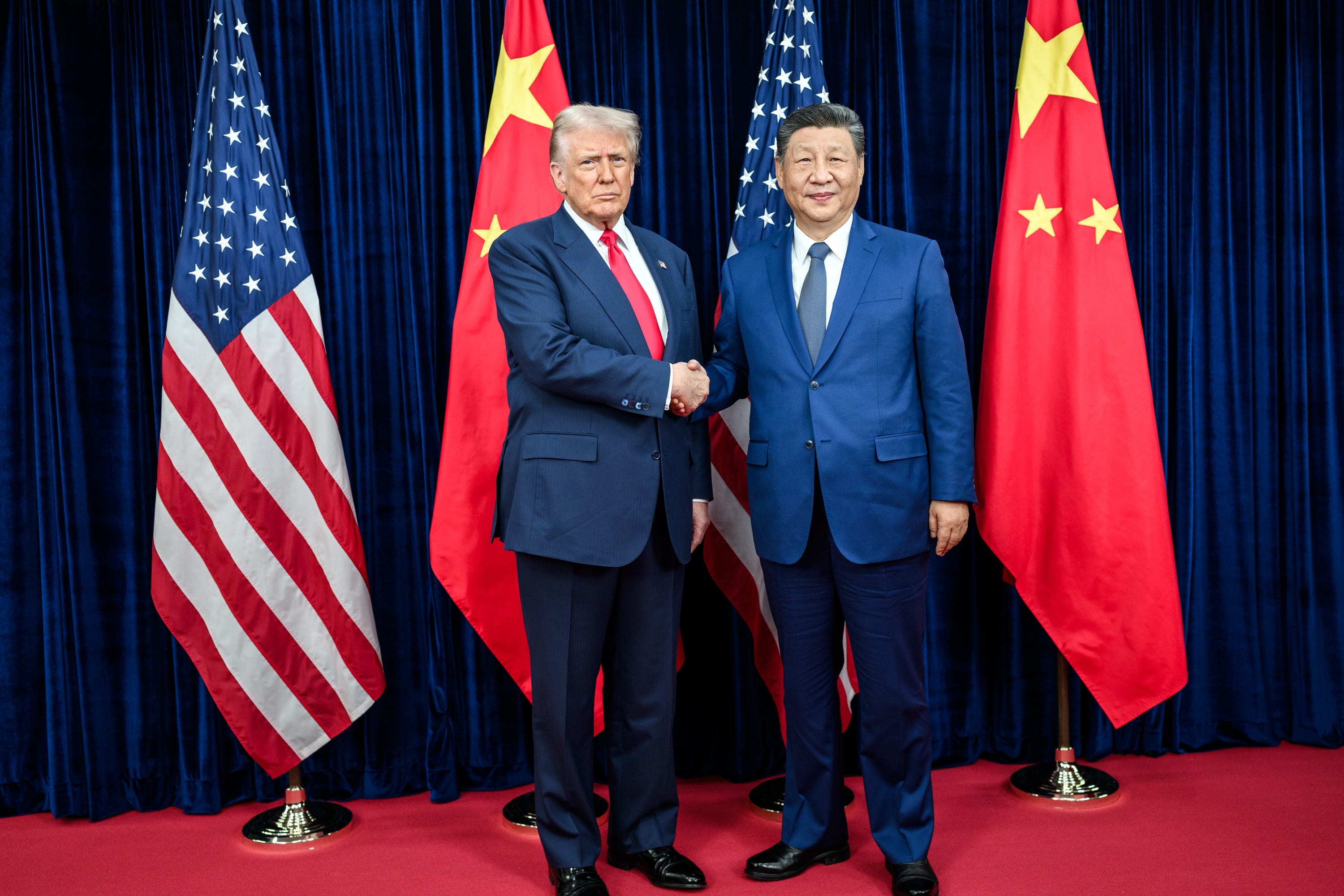

Image: President Donald Trump greets President Xi Jinping in Busan, South Korea, October 30, 2025. Source: The White House.

Donald Trump and Xi Jinping met in Busan, South Korea, on October 30, 2025—their first face-to-face since Trump’s return to the White House. The context was combustible: months of tariff brinkmanship, Chinese counter-tariffs and rare-earth export curbs, and a widening web of U.S. technology controls. Trump arrived brandishing threats of still-higher duties and broader restrictions; Beijing arrived signaling patience and conditional cooperation. The summit stretched beyond schedule and produced a narrow roster of deliverables. The atmospherics were exuberant—Trump called it “a 12 out of 10”—but the substance mostly restored a tense equilibrium.

What Was (and Wasn’t) Agreed

Tariffs: Washington will trim average duties on Chinese imports—from roughly 57% to 47%—largely by halving the “fentanyl-linked” levy.

Rare Earths: Beijing will delay the next tranche of rare-earth export controls for one year, easing short-term pressure on U.S. manufacturers.

Agriculture: China will resume large U.S. soybean purchases, offering relief for farm states while retaining discretion over volumes and timing.

Fentanyl: Both sides pledged cooperation on precursors and trafficking, with operational specifics still to be worked out.

Notably unresolved: Taiwan, the future scope of advanced chip and AI-hardware restrictions, and the long-term architecture of export controls.

Why Beijing Won

Drama vs. Positioning

Trump played for spectacle and quick wins; Beijing played for structure and time. China’s concessions—postponing controls and buying soybeans—are reversible and calibrated. They relieve immediate U.S. pain points without surrendering systemic leverage.

Concessions that Cement the Status Quo

Cutting the average tariff to the high-40s leaves duties at historically elevated levels. Soybean purchases restore a familiar trade valve rather than inaugurate a new equilibrium. Rare-earth curbs aren’t revoked, merely deferred. In effect, China reset the board to pre-crisis “hard normal,” not détente.

Strategic Questions Deferred

The real contests—on technology transfer, advanced chips, and the security perimeter around Taiwan—were skirted. That deferral signals two things: China can absorb pressure without altering core ambitions; and Washington is still defining which economic tools serve strategic ends, rather than just produce headline “wins.”

Narrative Control

Trump declared triumph; Beijing projected steadiness. For many hedging middle powers, predictable method is preferable to mercurial muscle. The contrast burnishes China’s image as a patient negotiator even as it keeps its coercive options open.

The Strategic Calculus

Leverage vs. Threat: U.S. threats (tariffs, tech controls) became bargaining chips. Each conversion of a threat into a concession narrows Washington’s future options.

Tactical Wins vs. Strategic Gains: The U.S. gained visible relief; China kept structural advantages—control over critical inputs and chokepoints.

Decoupling vs. Interdependence: By dialing down tariffs rather than widening tech access, Washington tacitly acknowledged limits to full decoupling; Beijing highlighted the resilience of interdependence it can modulate.

Alliances vs. Bilateralism: Trump’s preference for leader-to-leader deals unsettles allies and opens space for Chinese multilateral courtship—especially across the Global South and resource suppliers.

Implications

This is a pause, not peace. Supply chains get a breather; markets exhale; farm states cheer. But the underlying rivalry deepens as both sides refine toolkits—Beijing perfecting selective coercion over critical minerals and market access; Washington sharpening targeted technology controls and outbound investment regimes. The danger is a stair-step escalation: each “truce” that leaves fundamentals untouched raises the pressure required to move the other side next time.

What to Watch Next

Tariff Trajectory in 2026: Does the Trump administration bank the tariff cut—or snap back if fentanyl metrics and soybean volumes disappoint?

Rare-Earth Clock: How industry hedges during the one-year reprieve—inventory builds, allied sourcing, or accelerated magnet supply outside China.

Tech Controls 2.0: Whether Washington tightens rules on AI accelerators, cloud access, and toolchains—and how Beijing retaliates beyond minerals.

April 2026 Visit: If Trump’s planned Beijing trip materializes, does it deliver structural trade-tech guardrails, or simply tradeables-for-optics 2.0?

Allied Signaling: Whether Japan, the EU, and South Korea align on critical-minerals and chip controls—or pursue hedging compacts with China.

Our Take: The Busan summit illuminated three thresholds. First, the tariff threshold: below ~50%, duties become tradable currency, not punishment—inviting cycles of performative escalation and negotiated partial rollback. Second, the chokepoint threshold: rare earths and magnets remain Beijing’s quiet scalpel; even a delay advertises its capacity to cut. Third, the alliance threshold: every bilateral splash that bypasses allied coordination erodes the credibility of a unified economic front. The risk ahead is threshold creep—where temporary fixes normalize coercive tools, making the next rupture more dangerous and the off-ramps narrower.